Worker Reclassification Impact on Employee Benefits

Posted June 27, 2024

On Jan. 10, 2024, the U.S. Department of Labor (DOL) issued a final rule implementing a tougher analysis for worker classification under the Fair Labor Standards Act (FLSA). This change is expected to result in more workers being classified as employees, not independent contractors. This is significant because it provides more individuals with FLSA rights and protections, including overtime pay protections.

On Jan. 10, 2024, the U.S. Department of Labor (DOL) issued a final rule implementing a tougher analysis for worker classification under the Fair Labor Standards Act (FLSA). This change is expected to result in more workers being classified as employees, not independent contractors. This is significant because it provides more individuals with FLSA rights and protections, including overtime pay protections.

Employers who reclassify workers as employees should consider how this change impacts their employee benefits, including their compliance obligations under the Affordable Care Act (ACA). Workers who are reclassified may be eligible to participate in their employer’s employee benefit plans, depending on each plan’s terms and the employee’s position. Also, smaller employers may become subject to additional compliance requirements by reclassifying workers, such as:

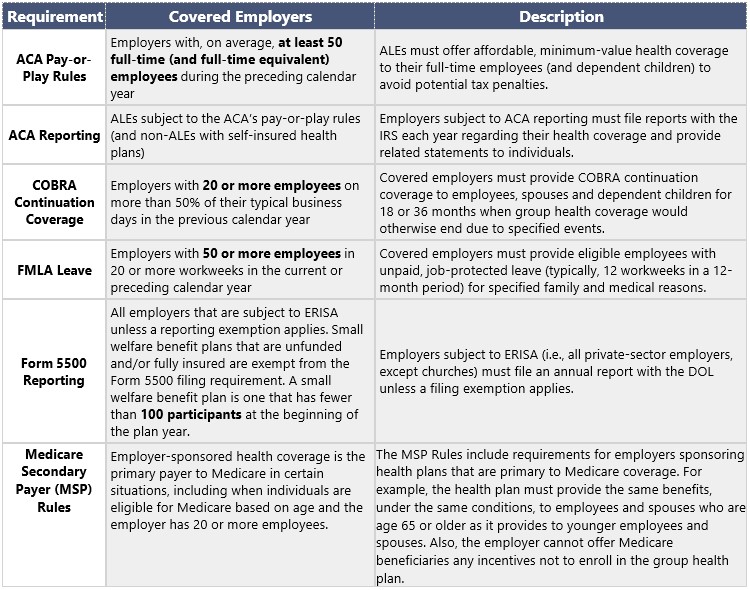

- The ACA’s “pay-or-play” rules for applicable large employers (ALEs);

- COBRA continuation coverage;

- Job-protected leave under the Family and Medical Leave Act (FMLA); and

- Annual Form 5500 reporting.

Additional compliance requirements may apply under state and local laws, such as state paid leave laws.

Action Steps

Employers reclassifying workers as employees should consider whether the workers now qualify for coverage under their employee benefit plans, which will likely increase overall employer spending. Employers should also analyze whether increasing employee numbers triggers additional compliance responsibilities under federal, state and local laws.

Worker Classification

Correctly classifying workers as employees or independent contractors is essential for an organization to comply with various federal, state and local laws. In general, independent contractors do not receive the same benefits and protections under the law as employees. Also, employers are not required to withhold or pay taxes on payments to independent contractors.

Misclassifying an employee as an independent contractor can have serious financial and legal consequences for an employer, including unpaid overtime pay, back taxes, interest and penalties, unpaid benefits and other legal damages.

The DOL’s final rule applies six economic reality factors to analyze employee or independent contractor status under the FLSA. These six factors include:

- The opportunity for profit or loss, depending on managerial skill;

- Investments by the worker and the potential employer;

- The degree of permanence of the work relationship;

- The nature and degree of control;

- The extent to which the work performed is an integral part of the potential employer’s business; and

- The worker’s skill and initiative.

Under this analysis, the economic reality factors are all weighed to assess whether a worker is economically dependent on a potential employer for work according to the totality of the circumstances. The final rule only revises the worker classification analysis under the FLSA. It does not apply to other laws—federal, state or local—that use different standards for worker classification. Although the DOL’s new analysis for worker classification under the FLSA does not apply directly to employee benefits laws, it is expected that more workers will be classified as employees under this new standard.

Impact on Employee Benefits

Generally, independent contractors should not be allowed to participate in an organization’s employee benefit programs due to their nonemployee status. Employers who reclassify workers as employees should review their benefit plan documents to determine each worker’s eligibility for benefits. For example, workers who are reclassified may be eligible to participate in their employer’s health and retirement plans.

ERISA’s fiduciary rules require employers to follow the terms of their employee benefit plan documents, including the rules for eligibility and contributions. Employers have some flexibility to exclude certain categories of employees from participating in their employee benefit plans in certain situations—for example, it is common for employers to exclude part-time employees from health plan coverage. However, employers should be cautious about creating new eligibility rules as there are limits on who may be excluded from participation. Also, many employee benefits are subject to annual nondiscrimination testing to ensure the coverage does not impermissibly favor highly compensated employees.

Additionally, if an employer is an ALE under the ACA, it must offer affordable, minimum-value health coverage to its full-time employees (and dependent children) or risk tax penalties. Both health plans and retirement plans are subject to limits on waiting periods for participation, and retirement plans cannot exclude part-time employees who meet certain service-based thresholds. Employers should be aware that, beginning in 2024, they must allow “long-term part-time employees” to make deferrals under their retirement plans, such as 401(k) plans. This includes employees who work for at least 500 hours of service over three consecutive years (two consecutive years, beginning in 2025).

Smaller employers who reclassify workers as employees should monitor whether the increase in their employee headcount triggers any additional compliance obligations under federal, state and local laws. The following federal employee benefit requirements may be triggered by an increase in employee numbers: